Planning is the key to successfully and legally reducing your tax liability. We go beyond tax compliance and proactively recommend tax saving strategies to maximize your after-tax income. Our consultants make it a priority to enhance their mastery of the current tax law, complex tax code, and new tax regulations by attending frequent tax seminars. Businesses and individuals pay the lowest amount of taxes allowable by law because we continually look for ways to minimize your taxes throughout the year, not just at the end of the year.

With the growing complexity & diversity of available options for tax planning purposes, it is important that we critically examine and bring across to you the new generation options available for investors in the present investment market.

There are various provisions in the Income Tax Act to save tax. The saving schemes one should opt. For would depend on the persons income and the tax bracket he / she is in.

Tax Deductions Through Investments According to Section 80C of the Income Tax Act, you can reduce your taxable income by Rs.1 lakh by investing in certain investments. These investments can be from any one source or a combination of sources such as Public provident fund, national savings certificate, tax saving mutual funds, pension plans, fixed deposits and life insurance policies. Since, the returns on investment, risk factors, term of deposit and entry load or commissions vary for each type of investment; here is some information about each type to help you select the best according to your needs. They are arranged as the best investments for young salaried tax payers in India according to the ones which I prefer the most –

.webp)

High Risk. Also known as tax saving mutual funds, an ELSS has the lowest lock in period of 3 years. As the money invested in an ELSS is invested by mutual funds in diversified stocks in the stock market, there is no guaranteed return. Dividends and profits from redemption of units after the term period is tax free.

Early life investment in the best life insurance coverage serves as a safety net in such a situation. The insurance company is required by the definition of life insurance to pay the nominee or beneficiary the pre-specified sum assured. As a result, his family is safeguarded even when the policyholder is not present.

Low Risk. Only investments made in scheduled banks for a period of five years or more can be counted as a Bank Fixed Deposit. The interest on such fixed deposits is around 8-9 percent. Income from interest is taxable. Forms are available at bank and post office counters.

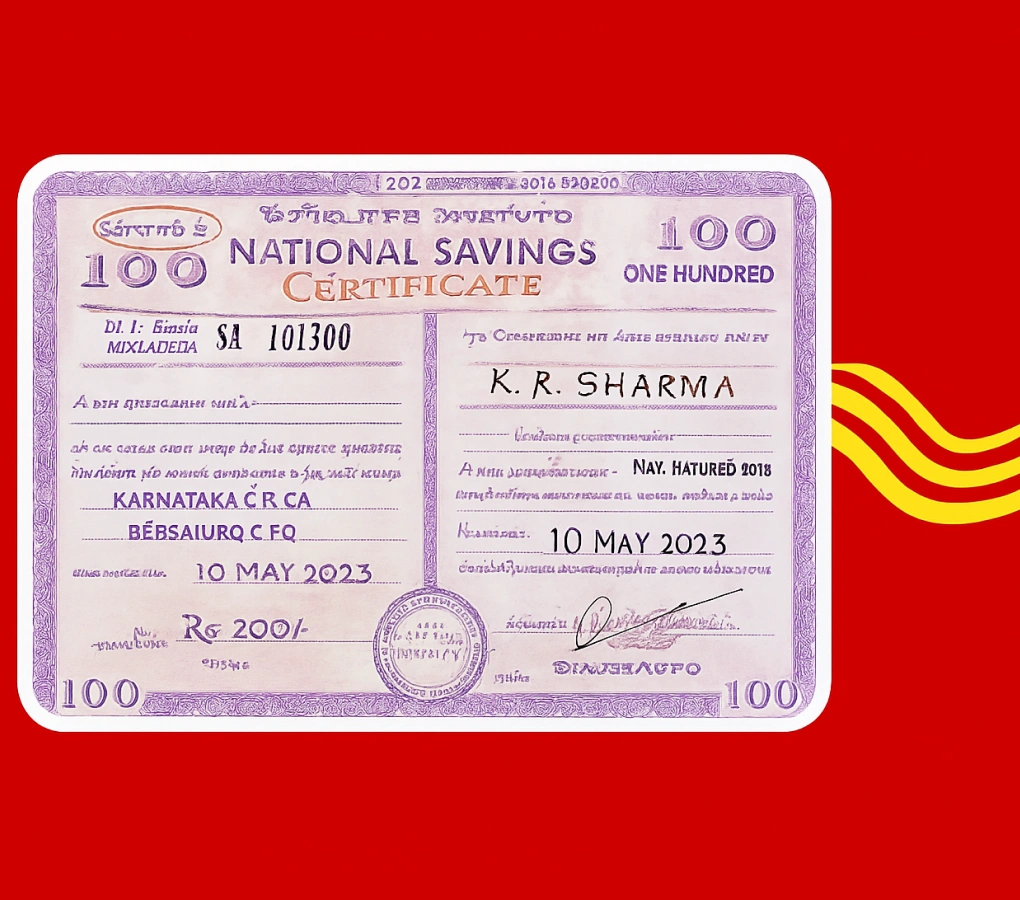

Low Risk. It comes in denominations of Rs.100, 500, 1000, 5000 and 10,000. The forms are available at any post office. The maturity period is six years while the interest rate is 8 percent compounded half yearly.

If you pay in cash, you will be given the National Savings Certificate then and there. If you pay by cheque, you will have to wait a week before you can collect the NSC certificate from the post office. Interest is taxable.

Low Risk. The main problem about these tax saving bonds are that they are open and available only for a fixed period. As many bonds open around February, they miss the January 31 deadline of submitting investment proof prevalent in most offices. The major institutions that offer these bonds are ICICI, IDBI and Rural Electrification Corporation.

Term periods can range from five to seven years and interest may vary from 6 to 9 percent per annum. Forms for Tax Saving bonds are available at local distributors that sit on the pavement outside major banks. Companies like ICICI have not come out with tax saving infrastructure bonds for a long period now.

Low Risk. The investment limit is Rs.500 to Rs.70,000 per year - in multiples of Rs.5. The main problem about this scheme is that you have to remember to invest an amount of at least Rs.500 annually for 15 years or your account will become defunct. Interest rate is 8 percent per annum compounded while the lock in time period is15 years. Another negative point is that as interest rates are on the downside and they are routinely changed by the government they may see a further fall.

As interest for the financial year is calculated on the lowest balance after March 5th, make sure you invest before that date. PPF Accounts may also be made in name of your spouse or kids for tax benefit. You can open a Public Provident Fund Account at main post offices, branches of the State Bank of India and some nationalized banks.

High Risk. Life insurance companies such as LIC, Tata AIG Life, Aviva, ICICI Prudential and BhartiAxa Life offer such pension plans. On maturity, the investor receives one-third of the amount while the remaining 2/3rd goes into an annuity that provides regular income in the form of pension. Only premiums till Rs.10,000 per year are eligible for deductions from total income.

Like Unit Linked Insurance Plans (ULIP’s), a substantial amount of the money invested into Pension Plans goes into paying ‘fund charges’ and commissions. Plus, the annuity received by the insured investor is taxable. Terms can extend from 10 years upwards. Though some return may be guaranteed – a large part depends on the debt market, share market and inflation.

A Unit Link Insurance Policy (ULIP) is one in which the customer is provided with a life insurance cover and the premium paid is invested in either debt or equity products or a combination of the two. In other words, it enables the buyer to secure some protection for his family in the event of his untimely death and at the same time provides him an opportunity to earn a return on his premium paid. In the event of the insured person’s untimely death, his nominees would normally receive an amount that is the higher of the sum assured or the value of the units (investments).

To put it simply, ULIP attempts to fulfill investment needs of an investor with protection/insurance needs of an insurance seeker. It saves the investor/insurance-seeker the hassles of managing and tracking a portfolio or products. ULIPs have been selling like proverbial ’hot cakes’ in the recent past and they are likely to continue to outsell their plain vanilla counterparts going ahead

Only people over the age of 60 years and retired personnel over 55 years are allowed to invest in this scheme. This scheme is available at all public sector banks in the country. Investments have to be made in multiples of Rs.1000 till a maximum of 15 lakhs for a period of five years

The deposit made gets an interest of 9 percent per year from the date of deposit which is computed quarterly. Interest is taxable and is deducted at source

If you are repaying such a home loan, the principal amount of the loan taken can be counted as a deduction under Section 80C of the Income Tax Act.

The tuition fees of upto two children at school, college and university level may also be taken as a deduction from total income thus reducing the amount on which tax will be calculated.

According to Section 24, a tax exemption of up to Rs. 1,50,000 is allowed on the interest paid for a home loan in the current financial year

Section 80 D - An amount of up to Rs.15,000 for individuals and Rs.20,000 for senior citizens as premium towards a medical insurance or mediclaim policy is tax deductible. This also includes medical insurance for dependents such as spouse, children or parents on the condition that you paid the premium.

Section 80E - The yearly limit for deduction is Rs. 40,000 (for both the principal and the interest). Only loans taken for higher education - fulltime studies in any graduate or post-graduate, professional, and pure and applied science courses - may claim deduction. The deduction will be available for a maximum of eight years starting from the day you start repaying the education loan.

Section 80G – All donations to specific charitable organizations such as the Prime Minister’s Relief Fund, CARE and Help Age India are eligible for a 100 percent tax relief. Donations to other charitable institutions and trusts get only 50 per cent tax relief.

Copyright© . Powered by Yetlo Tech Private Limited | All Rights Reserved .